Skipton Building Society has introduced a groundbreaking 100% mortgage program for tenants who have trouble setting aside funds for a down payment. This represents the first no-deposit mortgage plan in the UK since 2008 that doesn’t require a guarantor. Let’s delve into the specifics of who qualifies, how it operates, and the potential hazards to keep in mind.

The 100% mortgage by Skipton is exclusively for first-time buyers who have consistently paid their rent in full and on time for at least a year. Skipton’s 100% mortgage is a five-year fixed-rate mortgage, similar to other fixed-rate mortgage deals in the market, where you pay the same interest rate for five years. However, the significant difference is that Skipton’s new offer doesn’t necessitate a down payment.

This mortgage targets tenants who find it hard to save for a deposit, especially considering the rising rents and property prices. To qualify, you must:

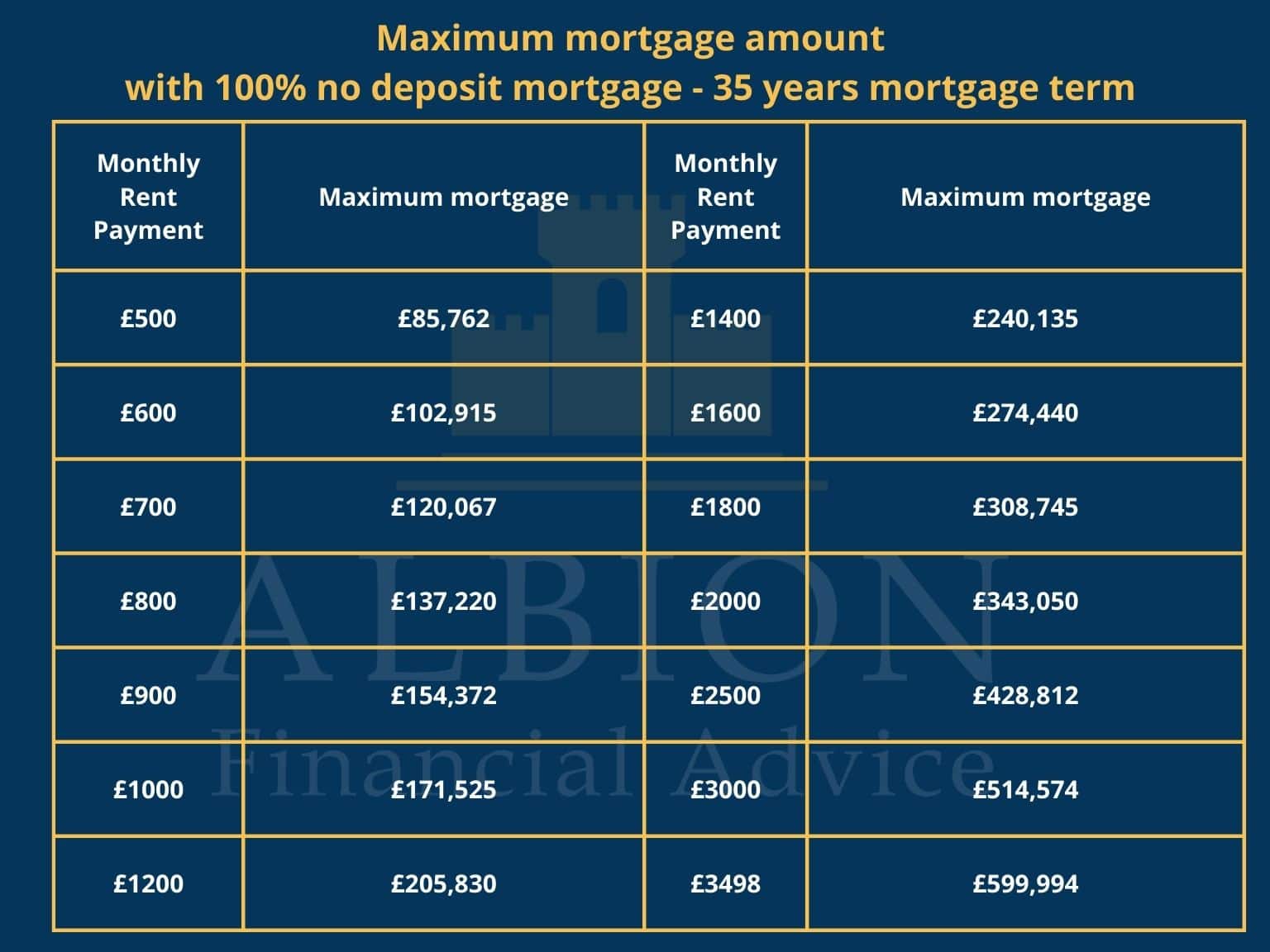

However, there’s a stipulation: the amount you can borrow must be equal to or less than your current monthly rent. While the typical mortgage loan amount is determined by your income, expenditures, and the lender’s affordability calculations, Skipton’s 100% mortgage caps the loan amount to not exceed your monthly rent. For instance, if you’re paying £1,000 per month for rent, you couldn’t borrow more than what would result in a monthly mortgage payment exceeding £1,000. The potential borrowing power based on your monthly rent is explained below.

While you may be paying £1,000 a month in rent, it doesn’t guarantee an equivalent loan amount with this mortgage. Skipton’s independent affordability assessments still need to be satisfied. If Skipton has any doubts about your repayment capacity, the lending amount may be reduced. The maximum you’re allowed to borrow is capped at £600,000.

Depending on the region you intend to live in and the property values there, this mortgage may not prove to be beneficial. As per the latest UK House Price Index, the average property bought by first-time buyers is priced at £238,000. To borrow this amount, your monthly rent should exceed £1,389.

Skipton’s 100% mortgage offering carries a 6.19% interest rate. It’s worthwhile noting how this stacks up against other options.

Skipton’s 100% five-year fixed mortgage has an interest rate of 6.19% and, uniquely, there are no accompanying fees. However, this could be viewed as a high price to pay for a no-deposit mortgage. Should you manage to gather a 5% deposit, you’ll find five-year fixed-rate mortgages at 95% Loan-to-Value (LTV) that are considerably less expensive at present.

In the face of these figures, it’s crucial to understand the risks involved, including the possibility of your mortgage ending up costing more than your property’s value. 100% mortgages are not only more expensive but carry a higher risk of negative equity. This occurs when your mortgage’s value exceeds your property’s value, a situation that could arise if property prices significantly decline.

With a 90% mortgage (thus, a 10% deposit), property prices would need to fall by more than 10% for you to risk negative equity. However, with a 100% mortgage, even a small drop in prices could lead to this situation.

Moreover, the newer your mortgage, the higher the likelihood of falling into negative equity if property prices fall. This is due to the fact that in the early stages of your mortgage, a greater portion of your monthly payments goes towards interest rather than principal reduction, keeping your LTV high for the initial few years.

Negative equity can significantly impact your financial situation, as it may hinder your ability to remortgage or relocate (given the limited availability of remortgage deals for those with 95% or higher LTV). If you’re unable to remortgage, you may be stuck with your current deal and unable to switch to a more cost-effective one.

Please note that the rate and all other data is valid on 01.10.2023 and can change at any time and might not be up to date in this post.

YOUR HOME MAY BE REPOSSESSED IF YOU DO NOT KEEP UP REPAYMENTS ON A MORTGAGE OR ANY OTHER DEBT SECURED ON IT.