Mortgage After a Debt Relief Order: What's Actually Possible in 2026

If you've been through a Debt Relief Order and you're wondering whether homeownership is still on the table - the answer is yes. Not "maybe eventually", not "only if you wait a decade". Yes, with a 15 per cent deposit, as little as 12 months after your DRO discharged.

That's not what most people expect to hear. The high street banks will turn you down flat - automated systems, no human involved, immediate decline. But there's a whole sector of specialist lenders that operates completely differently. They read your situation. They consider what happened and why. And some of them will lend at 85 per cent LTV to someone with a DRO on their file.

Worth being upfront about this: it's not straightforward, and the rates won't be pretty. But it's possible. This guide covers exactly how.

What you'll learn:

- Which lenders will consider a mortgage after a debt relief order - and at what deposit

- The 6-year rule and why the discharge date isn't the only date that matters

- What kills an application (one thing in particular)

- How income type affects your options

- When the high street becomes accessible again

Yes, You Can Get a Mortgage After a Debt Relief Order - Here's the Reality

The first thing most people discover, usually the hard way, is that every major high street bank uses automated credit scoring. Halifax, Santander, NatWest - all of them. The system sees a DRO on your file and issues a decline before a human ever looks at your application. No conversation, no context, no exceptions.

Specialist lenders work differently. Bluestone Mortgages, Norton Home Loans, Vida Homeloans - these are underwritten manually. A real person reviews your file, reads the circumstances, and makes a judgement call. They're not looking for perfection. They're looking for a coherent story: what happened, why it happened once, and evidence that your finances have stabilised since.

For a mortgage after a debt relief order, the key figure is 12 months post-discharge. That's the earliest point at which any UK specialist lender will consider you. And at that point, the minimum deposit on the market is 15 per cent.

That 15 per cent isn't available everywhere - only at Bluestone and, subject to interpretation, Norton. If you've got 25 per cent, more doors open. If you need to wait a bit longer, more doors still.

But 12 months post-discharge and 15 per cent deposit? That combination exists. It's not theoretical.

What a DRO Does to Your Credit File

A Debt Relief Order is a formal insolvency solution administered by the Insolvency Service. It was designed for people with serious debt - up to £50,000 - but without the assets or income to use bankruptcy or an Individual Voluntary Arrangement. To qualify, your disposable income after essential outgoings must be no more than £75 per month, and your total assets can't exceed £2,000 (with a separate allowance for a vehicle worth up to £4,000).

Once a DRO is approved, a 12-month moratorium period begins. Your qualifying debts are frozen. If your financial situation doesn't materially improve during that year, the debts are written off entirely and you're formally discharged. It happens automatically - no court, no further action.

Here's where the two important dates come in.

Date 1: The registration date. This is when the DRO was granted. From this date, the clock starts on the 6-year credit file window. Six years from registration, the DRO is legally removed from your Experian, Equifax, and TransUnion records - as if it never existed.

Date 2: The discharge date. This is 12 months after registration, when the moratorium ends and debts are cleared. This is the date specialist lenders use to calculate how long you've been "post-discharge".

So if your DRO was registered two years ago, you're currently one year post-discharge - and your credit file has four more years to run before the DRO drops off completely.

Both dates matter. The 6-year clock from registration determines when the high street becomes available. The post-discharge count determines which specialist lenders will consider you right now.

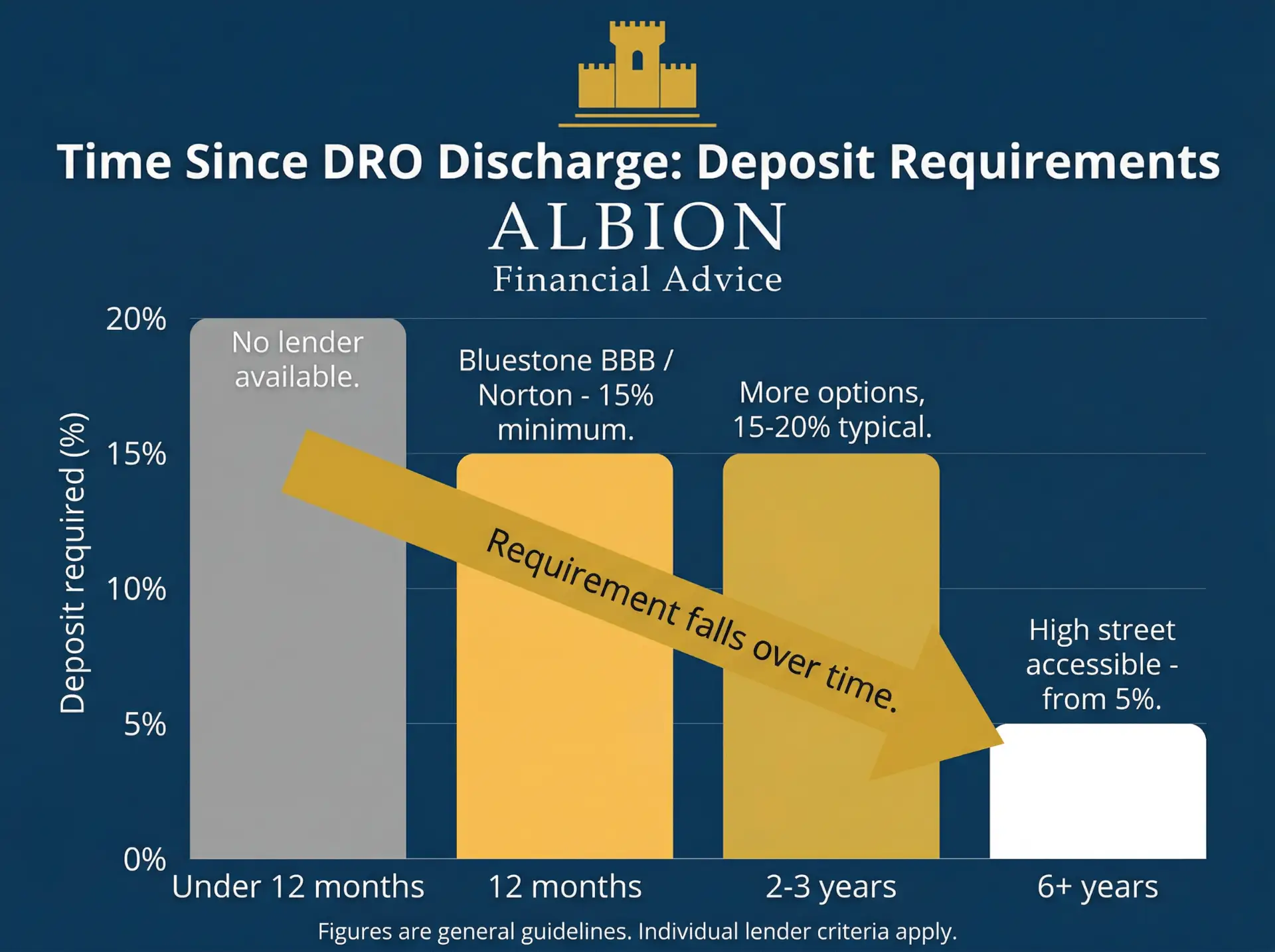

The Deposit Question: What 12 Months Post-Discharge Gets You

Deposit requirements for mortgage after a debt relief order are determined by how long you've been discharged. The specialist lending market uses a sliding scale:

- Less than 12 months post-discharge: No lender will consider you

- 12 months post-discharge: 15% deposit minimum - Bluestone BBB tier or Norton Optimal

- 2-3 years post-discharge: 15-20% typically; more lenders available

- 3-6 years post-discharge: 10-15% deposit; mid-tier specialist lenders enter the picture

- 6+ years post-discharge (DRO off file): High street accessible; 5-10% deposit possible

The 15 per cent option at 12 months is the floor. It's what the market currently offers, and it comes with conditions - but it's real.

Bluestone Mortgages: The Primary Route

If you're 12 months post-discharge and looking at a mortgage after a debt relief order, Bluestone is almost certainly the first conversation to have.

Bluestone doesn't use automated credit scoring. Instead, they have a tiered product structure - Clear, AAA, AA, A, BBB - based on the recency and severity of adverse credit events. An applicant one year post-DRO discharge typically lands in their A or BBB tier. The BBB tier supports up to 85 per cent LTV. That's a 15 per cent deposit.

Here's the thing about Bluestone's approach: they look at what's happened since the DRO, not just the DRO itself. Your conduct in the 12 months since discharge carries serious weight. That's what separates someone who qualifies at 85 per cent LTV from someone who doesn't.

What Bluestone needs to see:

- Zero payday loans. Not "none recently" - none at all post-DRO. Any payday loan after discharge is effectively fatal to the 85 per cent LTV route.

- No more than two missed payments on any active unsecured credit in the last six months.

- Any unsecured balance over £500 must show the most recent payment made.

What Bluestone ignores - and this matters:

- Defaults from telecoms and utility providers: disregarded entirely.

- CCJs or defaults under £500: not counted against you.

This is significant. A lot of people who've been through a DRO have a mobile phone default or a small water bill marker on their file. At Bluestone, that's invisible. They're looking at the bigger picture.

The rate reality: Bluestone applies a 1 per cent interest rate loading to all products where a DRO, IVA, or bankruptcy has been discharged within the last six years. As of early 2026, indicative rates for the BBB tier at 85 per cent LTV ran at approximately 7.79-7.89 per cent before that loading is applied - always confirm current rates with your broker, as these move. The reversion rate after the fixed term often exceeds 8.65 per cent, so the plan to remortgage onto a better deal once you have more equity (and more years post-discharge) is important to build into the strategy.

At Albion Financial Advice, Dariusz Karpowicz works with clients in exactly this situation - checking whether the BBB tier is accessible before any application goes in, running a soft search where possible so there's no hard footprint on the credit file if the timing isn't right.

Norton Home Loans: The Backup at 85%

Norton Home Loans is the other specialist lender offering up to 85 per cent LTV - but with one important caveat about timing.

Norton's criteria state that a borrower "Bankrupt or subject to a Debt Relief Order within the last 2 years" is unacceptable. How you read that sentence matters. If "within the last 2 years" is measured from the DRO registration date - which was two years ago for someone who is currently 12 months post-discharge - then you may marginally qualify.

If Norton's underwriter calculates it from the discharge date, you don't qualify until you're 2 years post-discharge.

This ambiguity is why Norton is the backup rather than the primary route. Experienced specialist brokers who have working relationships with Norton's underwriting team know how to present the application and get a steer before committing. This is exactly why the broker relationship matters - not just the platform they put you on, but whether they can pick up the phone and have that conversation.

Norton's other conditions:

- Minimum credit score of 300 (their own scoring model)

- Maximum loan size of £350,000

- Minimum £300 financial surplus in the affordability calculation

- At 85 per cent LTV: a full physical valuation is required (automated valuations accepted only up to 80 per cent LTV)

Vida Homeloans: If You Can Put Down 25%

Vida operates a tiering system - Vida 36, Vida 24, Vida 6 - based on time since adverse events. For someone one year post-DRO discharge, none of the standard tiers apply. But Vida runs a separate Packager Tier, accessible only through a small group of approved specialist packager partners.

This route requires a 25 per cent deposit rather than 15 per cent. But the rates are somewhat lower than Bluestone's BBB tier, typically running at 6.99-7.44 per cent (without the 1 per cent loading that Bluestone applies). It's worth doing the maths: a lower rate on a higher deposit versus a higher rate on a smaller deposit - the right answer depends on your specific numbers.

The catch: you can't access Vida's Packager Tier yourself. It requires a broker who is an approved Packager Partner. Worth asking your broker directly whether they have this access.

What Vida's Packager Tier accepts:

- DRO if at least 12 months since discharge

- Previous repossessions if more than 3 years ago

- No maximum on the number of historical defaults or CCJs provided none were registered in the last 6 months

- Defaults and CCJs under £250 excluded from assessment entirely

What Kills a Mortgage Application After a DRO

There's one thing that comes up again and again in our experience working with clients who've been through financial difficulty: the payday loan problem.

A payday loan taken out after your DRO discharge is close to universally fatal for a specialist mortgage application. Bluestone requires zero payday loans post-DRO, full stop. Norton and Vida take a similar line. The reason is straightforward - specialist underwriters are trying to identify a financial recovery story. A payday loan after discharge suggests the recovery hasn't stuck, and that's a different risk profile entirely.

If you've used a payday lender since discharge, you're almost certainly looking at a significant wait - often 12 to 36 months from when the last payday loan was settled - before the 85 per cent LTV route reopens.

Other things that seriously damage your position:

- Missed payments on anything in the 12 months since discharge - mobile contracts, credit cards, utilities. The post-discharge period is scrutinised heavily. Every lender wants to see clean conduct.

- Active credit applications in quick succession (multiple hard searches in a short period)

- County Court Judgements registered since discharge

The pattern specialist underwriters are looking for is simple: something went wrong, it's explained and isolated, and since that point everything has been clean. The DRO itself is forgivable. The six months after it isn't the place to slip up.

What Income Types Work

This is an area where specialist lenders - particularly Bluestone - are considerably more flexible than people expect.

Employed: Standard route. Three to six months' payslips plus a P60. Overtime and bonus income is often scaled back in the affordability calculation (typically 50 per cent of non-guaranteed elements), but base salary is assessed at full value.

Self-employed after a DRO: Bluestone accepts one year's trading history, backed by three months' business bank statements. Most other specialist lenders want two years, so Bluestone is notably more accessible here. The self-employed route post-DRO isn't closed - it just requires a lender who understands that rebuilding a business and rebuilding personal finances often happen in parallel.

Day-rate contractors: Bluestone accepts this from day one of a new contract, provided there's a minimum of three months remaining. No need to have been contracting for years first.

Benefits income: Bluestone includes 75 per cent of qualifying benefit income - Working Family Tax Credit, DLA, Child Benefit, Carer's Allowance - provided it has at least two years of entitlement remaining and doesn't represent more than 30 per cent of total household income.

Not every income type fits every lender. If you're working with an unusual combination - say, part self-employed, part benefits - it's worth having a broker map which lenders will work with your specific income profile before anything is applied for.

The 6-Year Milestone: When Everything Changes

Six years from the date your DRO was registered, it's legally removed from your credit file. Experian, Equifax, TransUnion - all three. The slate is clean.

At that point, the high street becomes available. Halifax and Nationwide will consider applications up to 90 per cent LTV on standard affordability terms. Barclays opens up at 85-90 per cent LTV. Kensington Mortgages will go up to 95 per cent LTV for purchases.

This is a significant milestone. The rates available on the high street are materially lower than specialist rates - and the products are more straightforward. No 1 per cent rate loading, no manual underwriting scrutiny, no packager requirement.

The strategic question, if you're working your way towards year six, is when to apply. Apply too early (even a week before the 6-year mark) and the DRO is still on file. Apply at the right moment and you're walking into a different lending environment entirely.

At Albion Financial Advice, we work with clients who are approaching the 6-year milestone to plan the timing carefully - because getting this right can make a real difference to the rates you're offered and the products available to you.

If you're further away from that milestone and looking at your options in the meantime, our complete guide to buying a house in the UK with no deposit in 2026 covers some of the alternative routes people use while they're rebuilding their credit position.

Working With a Specialist Broker

Worth being direct about something: the specialist mortgage market isn't something you can navigate solo. Lenders like Vida's Packager Tier aren't accessible at all without the right broker. Norton's 2-year clause requires a broker who has the underwriting relationship to get a steer before applying. Bluestone's BBB tier requires knowing exactly which combinations of adverse credit history they'll accept at 85 per cent LTV - and that knowledge comes from having placed cases with them.

A whole-of-market specialist broker - one who works regularly with adverse credit cases - also protects your credit file. Every full mortgage application leaves a hard search. A failed application costs you a hard search and sometimes pushes you into a worse lending tier. The goal is to only apply when there's a strong basis for approval.

Dariusz Karpowicz at Albion Financial Advice specialises in exactly this area - working with clients who have a DRO, IVA, or other adverse credit history on their file, and finding the right lender for their specific combination of deposit, income type, and credit history. If you want to understand your options before committing to anything, that's the conversation to start with.

Where to Go From Here

The path through a DRO to a mortgage isn't short and it isn't free of complications. But it's a real path.

At 12 months post-discharge, with a clean conduct record since the discharge and a 15 per cent deposit, Bluestone Mortgages offers the best starting point on the market. Norton is the backup. Vida opens up if you can stretch to 25 per cent or prefer a slightly lower rate. And at 6 years, the high street comes back into reach.

The biggest risk isn't the DRO itself - it's what happens after it. One payday loan, a run of missed payments, a hard search on a declined application: these are the things that push the timeline back. The DRO can be explained. Conduct since discharge is harder to argue around.

If you're unsure where you stand, the most useful thing is a proper review of your current position - credit file, income, deposit, timeline - before anything is applied for. That conversation costs nothing and can save you from a hard footprint on your file from an application that wasn't going to work anyway.

This article is for informational purposes only and does not constitute financial advice. Mortgage eligibility depends on individual circumstances. Lender criteria and rates are subject to change - always verify current terms with a qualified broker before applying. Albion Financial Advice is a trading name of [FCA-registered firm details]. Your home may be repossessed if you do not keep up repayments on your mortgage.

Dariusz Karpowicz

Director & Mortgage Adviser

Dariusz is a seasoned adviser with 15+ years in financial services. He founded Albion Financial Advice after gaining experience with established brokers, and has helped over 5,000 clients secure their ideal mortgage and protection solutions.

Frequently Asked Questions

Thinking about your next move? Message us on WhatsApp

Get personal, no-obligation mortgage advice from our FCA-regulated team. We reply fastest on WhatsApp.

We reply fastest on WhatsApp, message us anytime.